undeniably the financing simulator it helps us a lot in the decision to buy a house or apartment, as we get accurate information on the financial market without leaving home.

In the past, this was impossible and to simulate financing it was necessary to go to the bank.

Certainly this need has been annulled, just using the internet we get the information we want.

In this way, we were able to simulate the best banks and determine the best option to finance a car.

Following this subject, today here in our article we will deal with the vehicle financing simulator.

We've put together a series of information that will certainly help you in this very important process that is making a loan.

How is the loan/financing calculated?

For you to discover calculation of your financing or loan, you will either need to do an online simulation, using a financing calculator (as you will see further down in this article) or you can choose to do an online simulation of the type of financing you intend to do.

In that case, you can go to the official websites of the respective banks.

But don't worry, below we will give you a comparison of the best banks for you to finance.

What is the finance simulator?

The financing simulator consists of a digital and online tool.

That allows you to know in detail the financing you are thinking of joining.

Undoubtedly, this mechanism is essential for those who want to save money, as it shows us which banks have the lowest rates on the market.

Without using this simulator, you will end up closing a deal with the company with the highest interest rates, which will result in expensive financing.

What is simple and compound interest?

First of all, it is necessary to understand that we will always pay interest, regardless of the financial transactions we choose.

However, it is necessary to understand how simple interest and compound interest work, in order to have a financial education that allows us to make smarter choices.

What we need to keep in mind is that there are two types of interest: simple and compound. See the explanation of each one below!

simple interest

In general terms, we can understand that simple interest is the one that incurs only on the borrowed amount, without adding any other element in the calculation. Let's see an example to better understand how this works?

Will we understand this in practice? Take a look: suppose you took out a personal loan in the amount of R$ 8,000.00 to pay with a rate of 3% per year. In this case, you would pay a total of R$ 8,240.00 (R$ 8,000.00 loan and R$ 240.00 interest).

Therefore, as we noticed, the interest was calculated only based on the R$ 8,000.00 that were borrowed, without changing in the 3 years of the contract.

Meet our simple interest calculator!

Compound interest

Now compound interest is completely different.

Other people also call it “interest on interest”.

Therefore, in this case, interest is recalculated in different financial intervals, focusing on interest already calculated previously.

In other words: interest is charged on amounts that already had interest. Hence the term “interest on interest”.

Let's practice: you financed a simple car worth R$ 10,000.00, with compound interest of 3% per year, therefore, within 3 years.

In the first year, you will have to pay interest equivalent to R$ 300.00 (3% of R$ 10,000.00). But for the second year, that amount would technically change, because that would be interest on interest.

Thus, the calculation base value would be R$ 10,300.00 (R$ 10,000.00 of the loan and R$ 300.00 of interest for the first year). So 3% of that would be R$ 309.00.

Finally, in the third year, the base value of the calculation would be R$ 10,609.00 (R$ 10,000.00 loan + R$ 300.00 interest for the first year + R$ 309.00 interest for the second year). Therefore, the payment in interest would be R$ 318.27.

To sum up everything we've said: in total, you would pay R$ 10,927.27 to the bank that financed your motorcycle, with R$ 10,000.00 for a loan and R$ 927.27 for compound interest.

Did you understand? If not, leave your comment at the end of this article.

Advantages of using the financing simulator

Why should I simulate before financing? You will have this answer by seeing below the advantages of simulating. Take these advantages as a basis and do not ignore them, and they are:

Discover all the opportunities previously

By choosing to simulate, you will get to know all the opportunities on the market, being able to sort by who is the best.

Possibility to compare rates and their effects in the future

Undoubtedly, interest rates are the ones that have the most effect on financing, which is why you cannot finance without studying the information.

With the simulator you will get to know interest rates and their effects on financing.

Get to know Digital Seguro's financing calculator

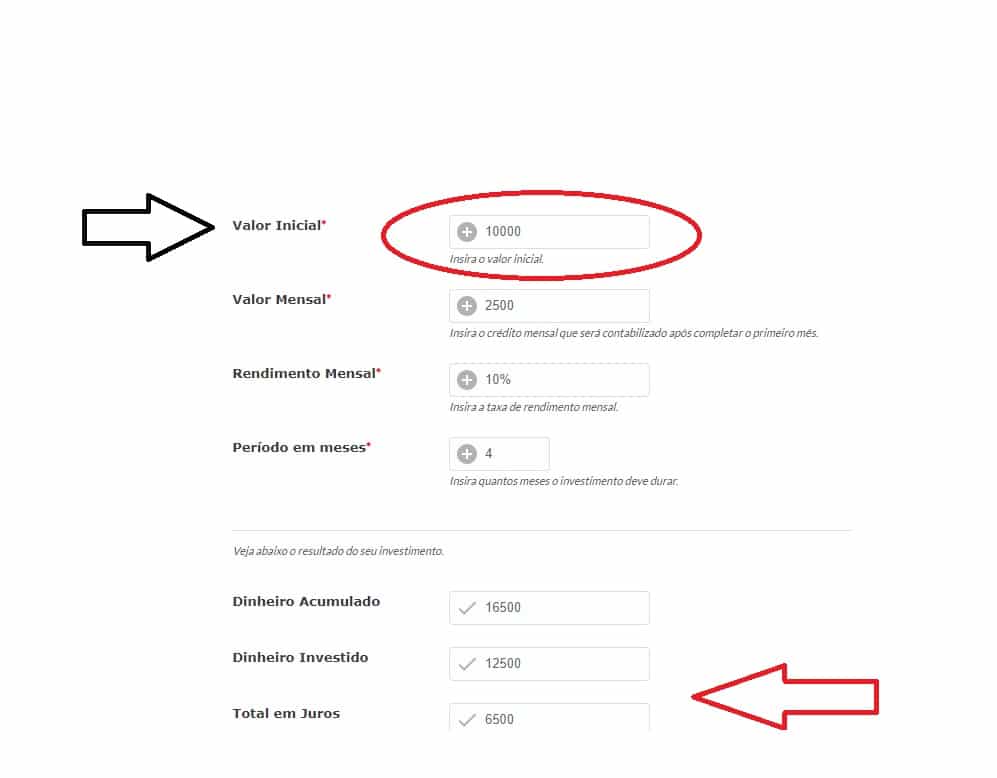

In order for you to be able to simulate financing, first you need to have a fixed amount that you need to do the simulations using our calculator that we have developed especially for you.

After that, go to their website and look for the simulator, so you can fill it out and get the results.

Check below how you can do a simulation using our Digital Insurance calculator.

Top financing simulator options

Santander Financing Simulator

You need to choose the value of the property, how much you want to finance and see the conditions that the bank has reserved for you. In the Santander Financing online simulation you will be able to find out about the bank's fees and interest. To know now, simulate here.

Itaú Financing Simulator

Bradesco Financing Simulator

Banco Bradesco also stands out in property or real estate financing, with it you can finance up to 80% of your asset, you can also do it in up to 30 years for payment.

Fast agility, that is, the response process does not take days.

Everything, thinking of you. To know more, simulate here.

Make your choice now!

Simulate, compare and opt for the best financing with Secure Digital.

Did you like it? Share!